Latin America’s video market is undergoing a structural transformation, with growth no longer driven by new household penetration but by increasing service density within existing homes.

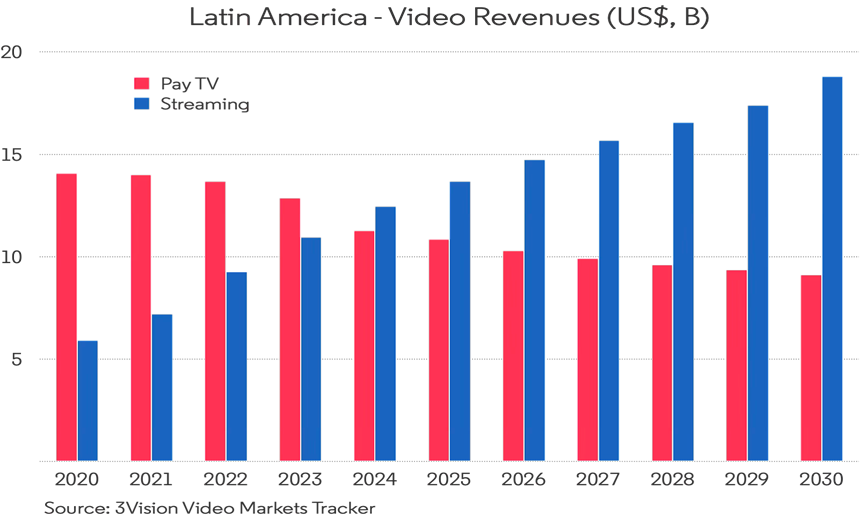

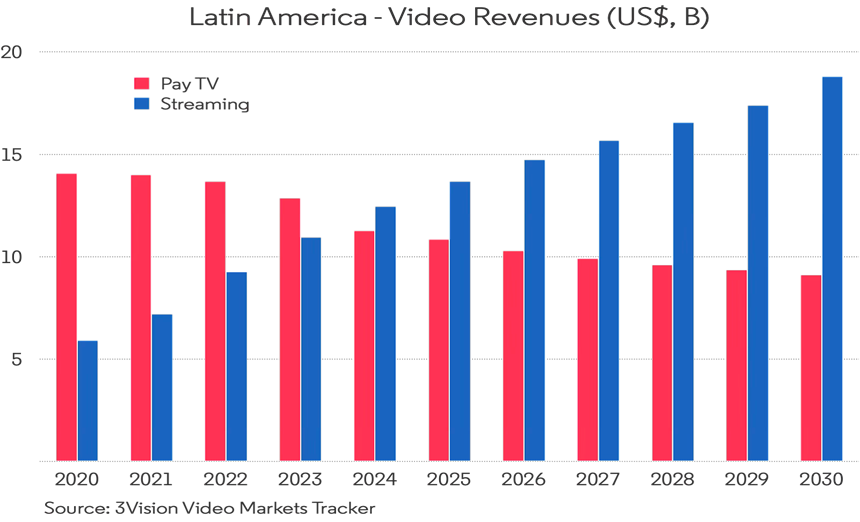

OTT (Over-the-Top) video revenues are projected to rise from $11 billion in 2023 to nearly $19 billion by 2030. By the end of the decade, OTT is expected to surpass Pay TV and become the region’s largest video revenue stream. The number of households subscribing to at least one SVOD service will grow from 66 million to 84 million.

However, the more significant expansion is internal: total SVOD subscriptions are forecast to climb from 111 million to 176 million, pushing the average number of subscriptions per paying household from 1.68 to over 2.0. In other words, growth is being driven not by penetration, but by density or “stacking.”

Advertising-supported models will play a central role in this evolution. AVOD revenues are expected to nearly triple, increasing from $2 billion to $6 billion, accounting for roughly half of total streaming growth. Meanwhile, FAST channels are projected to expand from $400 million to $1.6 billion, becoming an increasingly meaningful segment of the regional TV advertising market.

In 2024, Disney+ integrated Star+ into its core platform, signaling a broader strategy focused on reducing fragmentation and improving bundling efficiency. Netflix is anchoring its Latin American growth strategy around its ad-supported tier, while Max and Paramount+ are strengthening hybrid and telco-partnership models.

Meanwhile, Pay TV revenues are projected to decline from $13 billion to $9 billion by 2030. Although subscriber losses remain relatively moderate, falling ARPU continues to erode overall value.

The next phase of competition in Latin America will be defined less by household acquisition and more by which players can successfully balance subscriptions, advertising, and FAST offerings to monetize increasingly dense streaming households