The European Audiovisual Observatory released its 2024-based annual report analyzing top players in Europe’s audiovisual (AV) market.

The European Audiovisual Observatory report evaluates market concentration, revenues, public funding, pay-TV, SVOD, TV advertising, and in-video OTT advertising. Comcast, Netflix, and YouTube ranked as the top three AV players in Europe by operating revenue.

European companies still hold 56% of operating revenues among the top 100 AV groups, largely due to telco-driven entities. US-backed platforms dominate the high end of the market; one-third of top 10 AV revenues come from US companies.

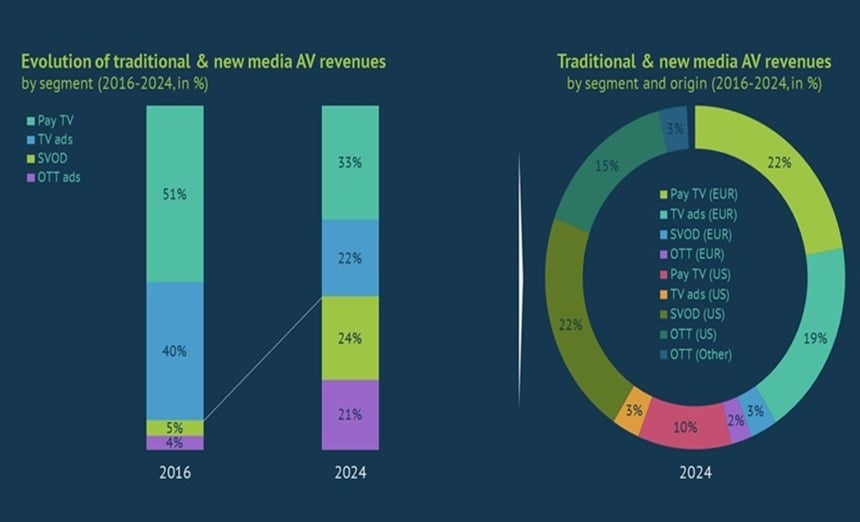

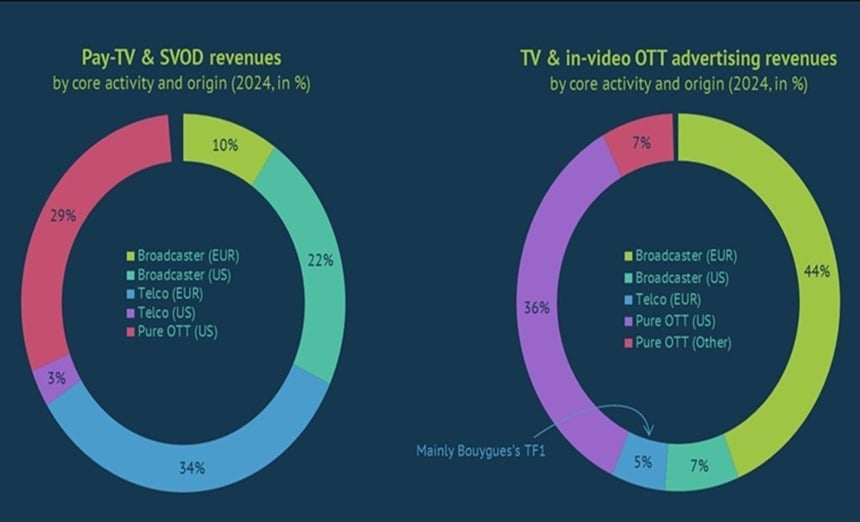

Between 2016 and 2024, US-backed firms’ market share increased by 9%, driven by OTT platforms and video-sharing services. Netflix overtook Sky in 2024 to become the leading pay-AV service provider, with SVOD accounting for around 40% of combined pay-TV and SVOD revenues.

Traditional TV and pay-TV still generate 70% of total pay-AV revenues, with European telcos capturing nearly 45% of total pay-AV revenues. In advertising, YouTube leads the combined TV and in-video OTT market; OTT ad revenue nearly matches traditional TV advertising volumes.

The European Audiovisual Observatory report highlights a structural shift: SVOD and in-video OTT now make up almost half of the AV market, segments dominated by non-European players. Overall, European groups remain strong in legacy media, but US-backed companies dominate fastest-growing segments of the audiovisual ecosystem.