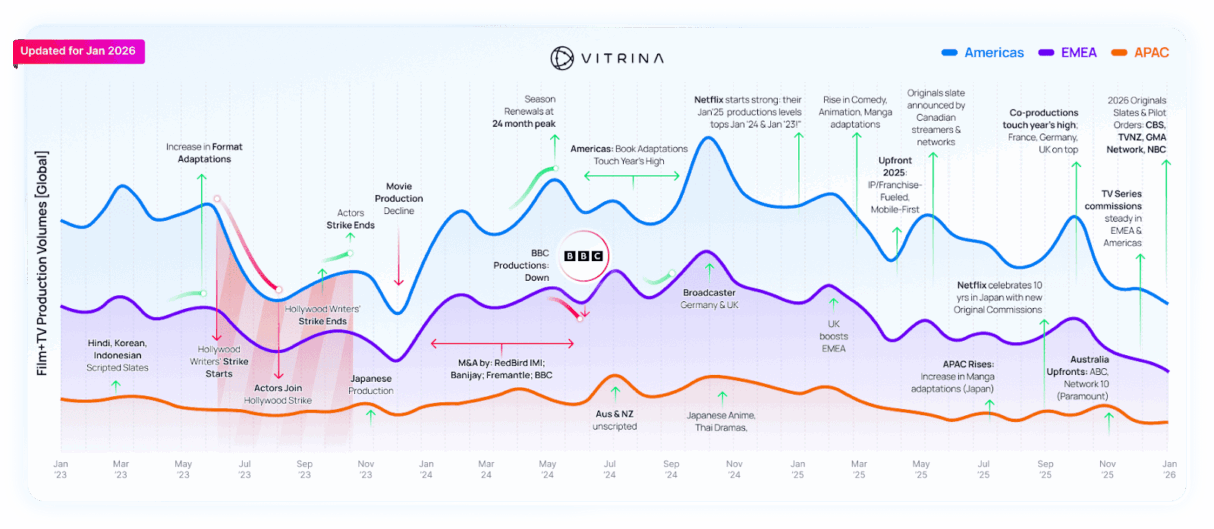

According to the global intelligence platform Vitrina AI, as of January 2026, global production trends show a strong shift toward proven intellectual properties (IP) and high-concept, localized scripted content to reduce market volatility.

In the Americas and EMEA, commissioners are favoring prestigious book adaptations and socially resonant dramas. Psychological thrillers like The Housemaid’s Secret and The Girl with the Dragon Tattoo, as well as ambitious historical epics such as Mistborn and Beirut 1931, are particularly prominent.

Western markets maintain a mix of scripted content alongside high-impact factual and event programming, whereas the APAC region remains heavily scripted, with around 90% of productions focused on original scripted content.

Graphic novel and manga adaptations, including Blue Lock and Gundam, are driving production volumes in Japan and surrounding markets, supporting both live-action and animation pipelines.

Historical context (2023–2025):

2023: Hollywood strikes almost halted scripted production in the US and UK, prompting a shift to unscripted formats and international markets.

2024: Markets cautiously stabilized, with regional production surges in Japan, ANZ, Germany, and Brazil, offsetting continued restraint from major broadcasters.

2025: The global supply chain largely steadied, but growth remained measured and IP-focused.

Americas: 82% of tracked projects are scripted and 74% in English. Renewals, franchise extensions, and recognizable book adaptations dominate. Platforms like Netflix, Prime Video, CBS, and NBC are doubling down on IP and franchises.

EMEA: 74% scripted, with a broader linguistic mix including English, German, French, and Arabic. Commissioning balances prestige drama with high-impact factual content. France, Germany, and Ukraine are central hubs for co-productions.

APAC: 90% scripted content, with manga and graphic novel adaptations fueling animation and live-action production. Sports, sci-fi, and fantasy genres are particularly strong.

Scripted content dominates globally, while original content is becoming secondary. IP-based franchises and adaptations are a strategic priority. The industry is moving away from the high-volume production approach of the Peak TV era, focusing instead on capital efficiency and long-term, franchise-driven content economies.